It is no shock that journey rewards bank cards get fairly a little bit of protection right here at TPG.

Making the most of prime welcome bonuses and strategically utilizing your playing cards for on a regular basis purchases can unlock improbable redemptions, equivalent to premium cabin flights and luxurious lodge rooms. Nonetheless, there are a variety of misconceptions about bank cards.

Let’s debunk one notable fantasy to hopefully aid you keep away from a credit score rating drop.

Associated: How do credit score scores work?

Fable: Closing a card I do not use will assist my credit score rating

There are a lot of explanation why you may need a bank card that you just do not use anymore.

Possibly it was the very first one you opened as an grownup, however you’ve gotten since been changed with a extra precious card. Possibly your priorities have shifted, and a sure card now not matches into your technique. Or perhaps you’ve gotten relocated to a brand new space of the nation and located that your go-to card has much less utility.

In these instances, you might suppose that you must cancel an unused card simply sitting in your pockets (or sock drawer) to assist your credit score rating. Nonetheless, in actuality, you might discover the precise reverse to be true. Canceling a card can really drop your credit score rating.

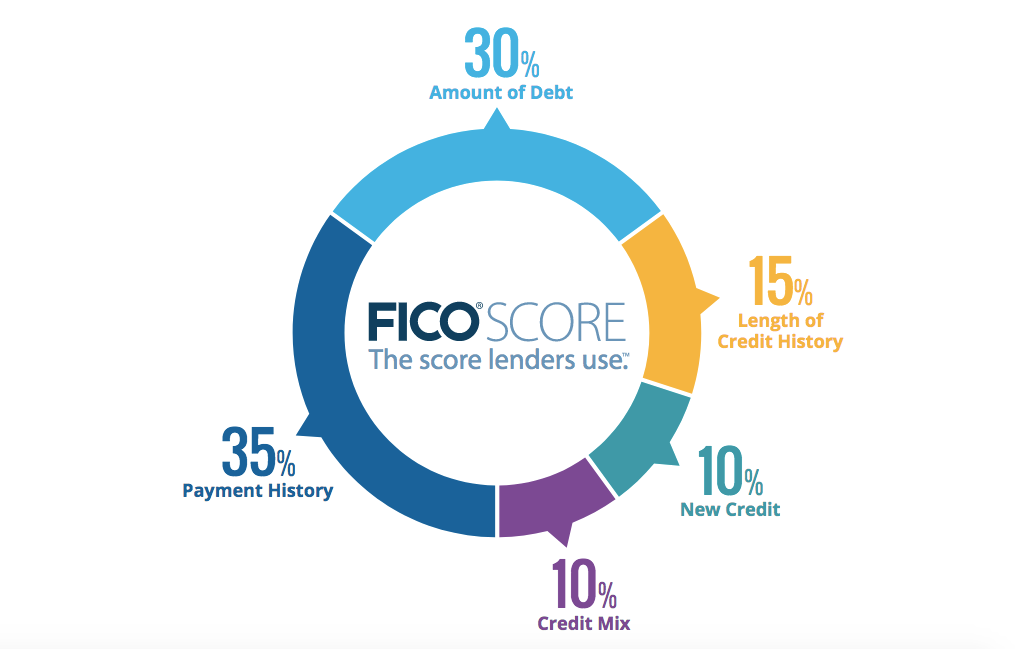

For this fantasy, it is important to grasp the various factors that contribute to your FICO rating, the metric most regularly used to find out your creditworthiness for any new line of credit score:

- Cost historical past

- Quantities owed

- Size of credit score historical past

- New credit score

- Forms of credit score used

Day by day Publication

Reward your inbox with the TPG Day by day publication

Be part of over 700,000 readers for breaking information, in-depth guides and unique offers from TPG’s specialists

Nonetheless, not all elements are created equal. Within the graphic under, these 5 elements are weighted based mostly on how necessary they’re to your rating.

In terms of closing a card you now not use, there’s one main issue that may influence your rating in a damaging means: quantities owed.

Associated: How you can test your credit score rating

Quantities owed

The second most necessary consider your FICO rating is your quantities owed — generally known as your credit score utilization charge. This appears to be like at how a lot of your credit score you’re really utilizing, and it is sometimes expressed as a share. This is the calculation: Complete stability in your account(s) divided by the whole restrict of account(s) equals utilization.

Conserving this quantity low exhibits issuers that you may successfully handle your credit score strains and are not vulnerable to overextending your self.

An instance

For example that you simply sometimes spend about $2,000 per 30 days in your main bank card with a $10,000 restrict, and also you at present have one other unused card, additionally with a $10,000 restrict. You thus have a utilization charge of 10% ($2,000 divided by $20,000).

Nonetheless, if you happen to then cancel that unused card, the month-to-month spending is now unfold throughout a a lot decrease credit score line. By canceling the cardboard, your utilization jumps to twenty%. That quantity is not too regarding, however you should not take something that impacts your rating evenly.

In fact, that is to not say that you must by no means cancel a bank card. In the event you’re now not utilizing a card that carries an annual price, it could not make sense to maintain that card open until the advantages you are getting outweigh the price. Simply you’ll want to name the issuer and inquire a couple of retention bonus. The agent could even be prepared to waive the annual price.

Associated: How canceling a bank card impacts your FICO rating

Size of credit score historical past

Whereas the quantities owed are the first issue affected by canceling a card you now not use, it may well additionally influence your credit score historical past, which makes up 15% of your credit score rating.

If the unused card is your longest-tenured account, canceling it may well negatively have an effect on the typical age of your accounts. Nonetheless, this does not occur straight away, as closed accounts (in good standing) will sometimes keep in your credit score report for as much as 10 years.

{kind=link}

However, canceling a card with no annual price — particularly one you’ve got had for years — can in the end influence your rating.

It is a key motive why I all the time suggest opening and holding not less than one card with no annual price. Simply you’ll want to make a least a number of purchases a 12 months on the cardboard to stop the issuer from canceling it as a result of inactivity. This may additionally assist forestall your factors and miles from expiring.

Backside line

There are a lot of myths about bank cards, and one widespread false impression is that you must cancel a card that you do not use anymore to spice up your credit score rating.

In actuality, this could have a major damaging influence in your credit score rating, as it’s going to decrease your general credit score restrict and thus improve your utilization charge. Over time, this might (doubtlessly) lower your common age of accounts as nicely. Whereas there could also be respectable causes to cancel a card, do not do it with out first contemplating the way it will have an effect on your credit score rating.

Associated: TPG’s 10 commandments of bank card rewards