{kind=link}

The U.S. economic system has entered Rasputin territory — it simply refuses to die.

Each time there’s something for individuals to fret about — conflict, inflation, industrial actual property, the Fed elevating charges, softening labor markets, and so forth. — the economic system takes it on the chin and retains transferring ahead.

At the moment we acquired one other strong jobs report. The unemployment charge truly ticked down once more to 4.1% and has been remarkably constant.1

It appears nearly foolish at this level to fret about probably the most dynamic economic system on the planet.

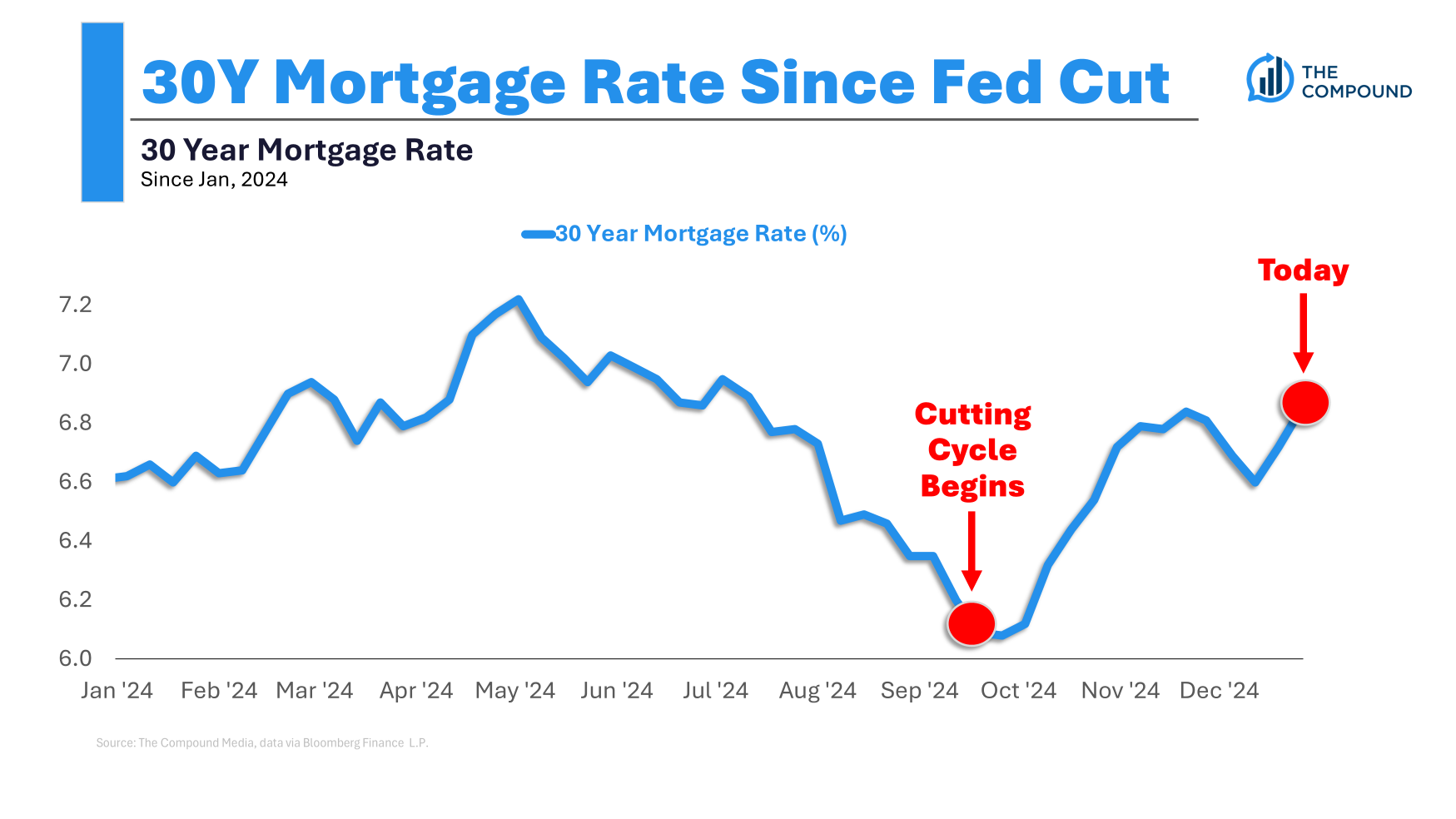

The truth that the Fed has been slicing charges ought to assist issues much more.

The issue is that whereas short-term charges on financial savings accounts, cash markets, CDs, T-bills and the like have gone down, borrowing prices have gone up for the reason that Fed began the present slicing cycle.

This one considerations me probably the most:

Everybody retains ready for decrease mortgage charges that by no means transpire.

Mortgage charges have been above 6% for two-and-a-half years now and it hasn’t actually mattered all that a lot.2 Housing costs proceed to hit new all-time highs as a result of so many owners locked in 3% mortgages through the pandemic.

There was some housing exercise in recent times however 55% of all owners nonetheless have a mortgage charge below 4% whereas practically three-quarters of borrowings are below 5%.

This, in fact, makes it tough for owners to purchase a brand new place as a result of the mortgage funds can be a lot greater. Simply take a look at the change in common month-to-month funds for the reason that begin of this decade:

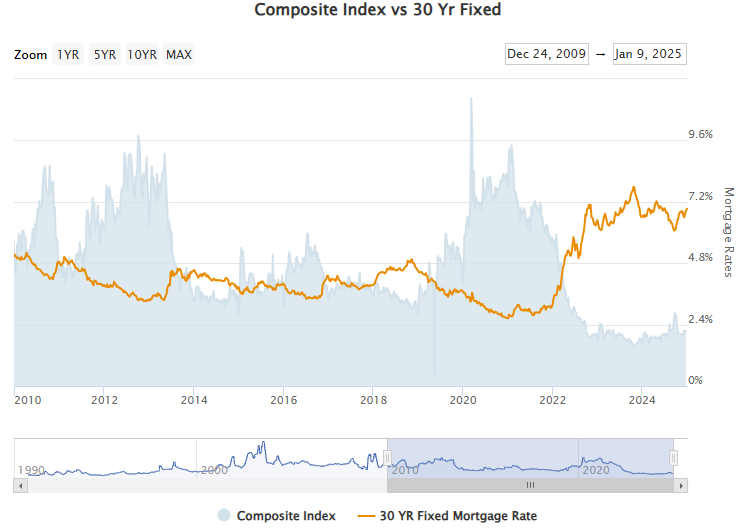

This all occurred so quick it is smart that there are fewer housing transactions. Simply take a look at the index of mortgage functions over time versus mortgage charges:

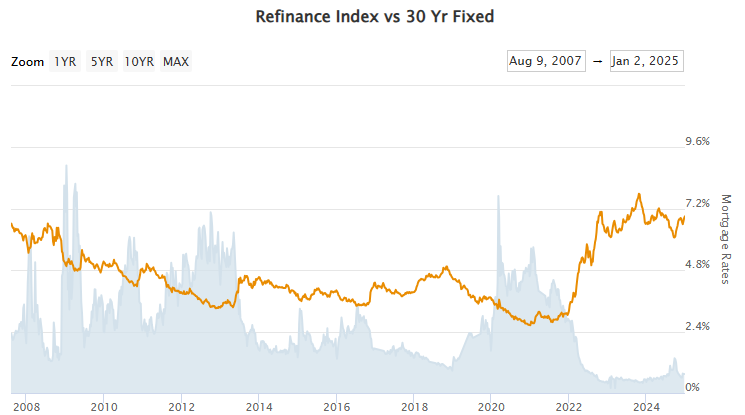

Nobody is refinancing both:

I’ve chronicled my worries about this many occasions previously. First-time homebuyers acquired a uncooked deal. They’re coping with greater housing costs and better borrowing prices concurrently via no fault of their very own.

However past homebuyers, my largest concern now’s what occurs to the remainder of the housing business if the present scenario persists.

Are you able to think about being a realtor on this surroundings the place transaction exercise has fallen off a cliff? Or how a few mortgage originator?

Housing exercise touches so many different areas as nicely. If you purchase a house you pay for realtor charges and shutting prices but additionally movers, inspections, value determinations, new furnishings, decorations, lawncare, and so forth. Plus, within the homebuilding course of you’ve got building staff, supplies, suppliers and permits.

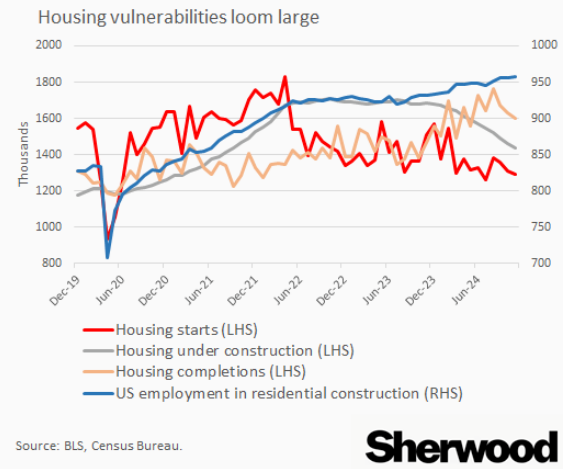

Luke Kawa at Sherwood information wrote a chunk just lately about how housing IS the enterprise cycle:

In a world the place potential new consumers are deterred by excessive long-term rates of interest, homebuilders are dealing with strain on margins thanks partly to making an attempt to subsidize a few of this charge sticker shock, and with administration of those corporations warning of lower-than-expected deliveries within the first quarter of 2025, employment in residential building stands out as a transparent vulnerability for the US job market.

Given the previous maxim “housing is the enterprise cycle,” popularized by a well-timed 2007 paper by Ed Leamer of the identical identify, meaning it’s an vital flashpoint for the US economic system and monetary markets as nicely.

Right here’s a very good chart from the piece exhibiting how exercise is rolling over:

Fortunately, the labor market stays robust however I don’t see how that may final until extra present owners do renovations.

Should you add up the entire parts which can be immediately or not directly tied to the housing market, it makes up one thing like 20% of GDP.

To date that hasn’t mattered to the general economic system but it surely has to finally if the established order stays.

The excellent news is the rationale for greater mortgage charges proper now’s as a result of the economic system stays robust.

The unhealthy information is it can in all probability take a weaker economic system to carry charges right down to a degree that induces extra exercise within the housing market.

Paradoxically, the treatment for top mortgage charges could be excessive mortgage charges in the event that they proceed to behave as a drag on the economic system.

Michael and I talked about mortgage charges, the housing market and rather more on this week’s Animal Spirits video:

Subscribe to The Compound so that you by no means miss an episode.

Additional Studying:

The Greatest Threat in Actual Property

Now right here’s what I’ve been studying these days:

Books:

1These are the previous 8 unemployment readings: 4.0%, 4.1%, 4.2%, 4.2%, 4.1%, 4.1%, 4.2% and 4.1%.

2Some individuals prefer to level out at present’s charges are near the long-term averages. And it’s true that the common mortgage charge since 1970 is greater than 7%. However homebuyers previously weren’t coping with housing costs that went up 50% in a 4 12 months interval.